【模型评价】理论与实现

source link: https://www.guofei.site/2017/05/02/ModelEvaluation.html

Go to the source link to view the article. You can view the picture content, updated content and better typesetting reading experience. If the link is broken, please click the button below to view the snapshot at that time.

【模型评价】理论与实现

2017年05月02日Author: Guofei

文章归类: 2-1-有监督学习 ,文章编号: 201

版权声明:本文作者是郭飞。转载随意,但需要标明原文链接,并通知本人

原文链接:https://www.guofei.site/2017/05/02/ModelEvaluation.html

对有监督模型的评价

- accurate

- stable 模型建好之后,输入一个样本,输出的预测值不能变来变去。 (对同一组样本同一模型,多次计算出的模型不能差别太大)

- general 推广性,对新样本预测效果同样良好。

- ease of use

- generat a fit ,建模比较方便(不用管,现在都快捷)

- measure accuracy,能否建立一个评价系统

- prediction

- swith algerithm,例如,神经网络有很多变种。

- share results,例如决策树的模型结果就可以很容易教给不懂模型的人

- Feature selection

- uncorelated predictor

- corelated predictor

针对回归模型的评价

MSE

R-square

Adjusted R square

针对分类模型的评价

混淆矩阵

- 模型输出的是预测结果

- 模型输出的是概率,这时用0.5截取

wikipedia这个table总结的很全,直接搬过来:

predicted condition

total population

prediction positive

prediction negative

Prevalence = Σ condition positiveΣ total population

true

condition

condition

positive

True Positive (TP)

False Negative (FN)

(type II error)

True Positive Rate (TPR), Sensitivity, Recall, Probability of Detection = Σ TPΣ condition positive

False Negative Rate (FNR), Miss Rate = Σ FNΣ condition positive

condition

negative

False Positive (FP)

(Type I error)

True Negative (TN)

False Positive Rate (FPR), Fall-out, Probability of False Alarm = Σ FPΣ condition negative

True Negative Rate (TNR), Specificity (SPC) = Σ TNΣ condition negative

Accuracy = Σ TP + Σ TNΣ total population Positive Predictive Value (PPV), Precision = Σ TPΣ prediction positive False Omission Rate (FOR) = Σ FNΣ prediction negative Positive Likelihood Ratio (LR+) = TPRFPR Diagnostic Odds Ratio (DOR) = LR+LR−

False Discovery Rate (FDR) = Σ FPΣ prediction positive Negative Predictive Value (NPV) = Σ TNΣ prediction negative Negative Likelihood Ratio (LR−) = FNRTNR

指标1

正确率 Accuracy (TP+TN)/total cases 误分类 Error rate=(FP+FN)/total cases指标2:P-R曲线

覆盖率 Recall(True Positive Rate,or Sensitivity) TPR = TP/(TP+FN) 命中率 Precision(Positive Predicted Value,PV+) PPV = TP/(TP+FP) F-score Fβ=(1+β2)TPR×PPVβ2PPV+TPRFβ=(1+β2)TPR×PPVβ2PPV+TPR P-R 曲线(Precision-Recall curve) 横坐标是TPR,纵坐标是PPV指标3:ROC曲线

TPR(True Positive Rate, sensitive, recall, hite rate) TPR = TP/P = TP/(TP+FN) FPR(False Positive Rate) FPR = FP/N = FP/(TN+FP) ROC曲线 横轴是FPR,纵轴是TPR AUC(Area Under the ROC Curve) ROC 曲线下方的面积。有些模型可以求出这个面积的统计量,称为R统计量

值得注意的是,在不同的场景中,选择的主要指标不同。例如:

覆盖率 Recall: 预测信用卡诈骗时,cover了多少骗子

命中率 Precision:精准营销时,发的宣传有多少人回应

在垃圾邮件分类时,错把一封正常邮件分类成垃圾邮件,这个结果的不良后果远高于错把一封垃圾邮件分类为一封正常邮件。

在医疗诊断时,错把患病诊断为未患病,其后果远比错发患病诊断为未患病严重的多。

对于多分类模型,指标可以有2种计算方法:

- 两两分解成n个二分类混淆矩阵,计算各个混淆矩阵的指标,然后对指标做平均

- 两两分解成n个二分类混淆矩阵,对TP,FP,FN,TN做平均,变成一个混淆矩阵,然后计算指标

比较两个模型时,可以用交叉验证得到每个模型的一组指标,然后对指标做两样本t检验,但这些指标有可能不独立。改进方法:用k fold 交叉验证,每次两个模型用同一组数据集,得到成对的指标,用配对样本t检验。

Lift

模型变化时,画出PV+曲线

衡量不同模型的预测能力

Brier评分

这个方法是某paper里面看到的,

BS=1N∑(p^−y)2BS=1N∑(p^−y)2

其中p^p^是模型输出的概率,y是实际结果。注意要计算所有选项

一个随机模型的BS=0.25,BS越小越好。

其它分析

正确性分析:(模型稳定性分析,稳健性分析,收敛性分析,变化趋势分析,极值分析等)

有效性分析:误差分析,参数敏感性分析,模型对比检验

有用性分析:关键数据求解,极值点,拐点,变化趋势分析,用数据验证动态模拟。

高效性分析:时间复杂度,空间复杂度分析

Python实现

主要指标

print(metrics.classification_report(test_target, test_est))#计算评估指标功能:

打印这四个指标:precision recall f1-score support

混淆矩阵

参见SVM

from sklearn import metrics

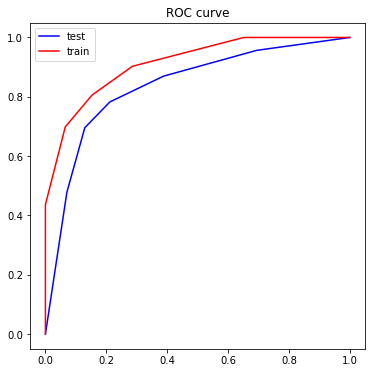

cm = metrics.confusion_matrix(y, y_predict) # 训练样本的混淆矩阵ROC

fpr_test, tpr_test, th_test = metrics.roc_curve(test_target, test_est_p)

fpr_train, tpr_train, th_train = metrics.roc_curve(train_target, train_est_p)

plt.figure(figsize=[6,6])

plt.plot(fpr_test, tpr_test, color=blue)

plt.plot(fpr_train, tpr_train, color=red)

plt.title('ROC curve')

功能:画出test set 和train set 的ROC图

其他评价1

见于kmeans方法

一套代码

参见SVM

1. 生成数据并导入包

import pandas as pd

import numpy as np

from sklearn import datasets, model_selection, preprocessing, metrics

X, y = datasets. \

make_classification(n_samples=1000, n_features=5, flip_y=0.1)

df=pd.DataFrame(np.concatenate([X,y.reshape(-1,1)],axis=1))

df.corr()

这里会打印相关系数矩阵,在进行流程之前看一下,对数据有个大概感觉

0 1 2 3 4 5 0 1.000000 0.584082 0.989028 -0.008031 -0.094029 -0.004766 1 0.584082 1.000000 0.697582 0.027633 0.753178 0.642409 2 0.989028 0.697582 1.000000 -0.002060 0.054074 0.112709 3 -0.008031 0.027633 -0.002060 1.000000 0.040401 0.015829 4 -0.094029 0.753178 0.054074 0.040401 1.000000 0.791798 5 -0.004766 0.642409 0.112709 0.015829 0.791798 1.000000

2. 划分训练集和测试集,并且特征工程

划分训练集和测试集

X_train, X_test, y_train, y_test = model_selection.train_test_split(

X, y, test_size=0.2, train_size=0.8, random_state=123)

简单的特征工程

这一步还应当包括异常值处理、无关特征剔除、降维等,相关内容在别的地方写了,这里重点写评价指标。

这里有个需要注意的点,test应当按照train来进行预处理,而不能用test的信息进行预处理。这两种做法都是错的:

- 先用全量数据做标准化,然后 train_test_split

- 先 train_test_split,然后在各自集合上各自做标准化。

min_max_scaler = preprocessing.MinMaxScaler()

min_max_scaler.fit(X_train)

X_train_scaled=min_max_scaler.transform(X_train) # fit_transform(train_data)可以两步一起做

X_test_scaled=min_max_scaler.transform(X_test)

3. 建模

这里展示简单的,实际工作中更为复杂。参见【sklearn】一次训练几十个模型

from sklearn import neighbors

model = neighbors.KNeighborsClassifier()

model.fit(X_train, y_train)

y_test_predict = model.predict(X_test)

y_train_predict = model.predict(X_train)

4. 评价

这里重点写评价指标

score

model.score(X_train, y_train), model.score(X_test, y_test)

混淆矩阵

metrics.confusion_matrix(y_test, y_test_predict, labels=[0,1]) # label可以控制显示哪些标签,用于多分类中输出类似这样

>>array([[97, 3],

[ 3, 97]])很多指标

- accuracy_score: metrics.accuracy_score(test_target, test_predict)

- precision_score:metrics.precision_score(test_target, test_predict)

- recall_score:metrics.recall_score(test_target, test_predict)

- metrics.f1_score(test_target, test_predict)

- metrics.fbeta_score(test_target, test_predict)

一次看完这些指标:

print(metrics.classification_report(test_target, test_predict))

precision recall f1-score support

0 0.97 0.97 0.97 100

1 0.97 0.97 0.97 100

micro avg 0.97 0.97 0.97 200

macro avg 0.97 0.97 0.97 200

weighted avg 0.97 0.97 0.97 200P-R曲线

metrics.precision_recall_curve(y_true, y_predict_proba)

ROC

import matplotlib.pyplot as plt

y_test_proba_predict = model.predict_proba(X_test)[:,0]

y_train_proba_predict = model.predict_proba(X_train)[:,0]

fpr_test, tpr_test, th_test = metrics.roc_curve(y_test==0, y_test_proba_predict)

fpr_train, tpr_train, th_train = metrics.roc_curve(y_train==0, y_train_proba_predict)

plt.figure(figsize=[6,6])

plt.plot(fpr_test, tpr_test, color='blue',label='test')

plt.plot(fpr_train, tpr_train, color='red',label='train')

plt.legend()

plt.title('ROC curve')

AUC

metrics.roc_auc_score(y_true, y_predict_proba)

metrics.roc_auc_score(y_train==0, y_train_proba_predict), metrics.roc_auc_score(y_test==0, y_test_proba_predict)

回归模型的评价指标

- 误差绝对值的平均值 metrics.mean_absolute_error(y_true,y_pred)

- 误差平方的绝对值(MSE) metrics.mean_squared_error(y_true,y_pred)

综合评价指标(图)

- 验证曲线 validation_curve,参数不同时,各个评价指标的曲线

- 学习曲线 learning_curve, 数据集大小不同时,各个评价指标的曲线

对交易模型的评价

金融中的交易模型,几乎都属于上面说的对回归和分类模型。因此,对回归和分类模型的评价同样适用。下面具体分析,其内容基本没有超越上文

- 这个系统是不是黑盒 如果模型的内在逻辑很难用业务逻辑解释,那么要打上一个问号

- 系统与实际的相符程度

- 测试数据是否覆盖一个经济周期

- 佣金&滑点是否准确地考虑进去了

- 测试结果是否有统计意义

- 交易次数越多,结果越可信

- 系统盈利越分散,结果越可信。否则,盈利太集中,说明有可能运气成分居多

- 是否有过拟合

- 参数越少越好。很多参数可能过拟合

- 魔法数字:为何是20日移动平均?为何不是30日或21日?

- 规则越简单,越不容易过拟合

- 对参数的敏感程度(不要参数稍小变动导致交易效果巨量变动)

参考文献

Wikipedia

您的支持将鼓励我继续创作!

Recommend

About Joyk

Aggregate valuable and interesting links.

Joyk means Joy of geeK