Report: Big U.S. Banks Are Stiffing Account Takeover Victims

source link: https://krebsonsecurity.com/2022/10/report-big-u-s-banks-are-stiffing-account-takeover-victims/

Go to the source link to view the article. You can view the picture content, updated content and better typesetting reading experience. If the link is broken, please click the button below to view the snapshot at that time.

Report: Big U.S. Banks Are Stiffing Account Takeover Victims

When U.S. consumers have their online bank accounts hijacked and plundered by hackers, U.S. financial institutions are legally obligated to reverse any unauthorized transactions as long as the victim reports the fraud in a timely manner. But new data released this week suggests that for some of the nation’s largest banks, reimbursing account takeover victims has become more the exception than the rule.

The findings came in a report released by Sen. Elizabeth Warren (D-Mass.), who in April 2022 opened an investigation into fraud tied to Zelle, the “peer-to-peer” digital payment service used by many financial institutions that allows customers to quickly send cash to friends and family.

Zelle is run by Early Warning Services LLC (EWS), a private financial services company which is jointly owned by Bank of America, Capital One, JPMorgan Chase, PNC Bank, Truist, U.S. Bank, and Wells Fargo. Zelle is enabled by default for customers at over 1,000 different financial institutions, even if a great many customers still don’t know it’s there.

Sen. Warren said several of the EWS owner banks — including Capital One, JPMorgan and Wells Fargo — failed to provide all of the requested data. But Warren did get the requested information from PNC, Truist and U.S. Bank.

“Overall, the three banks that provided complete data sets reported 35,848 cases of scams, involving over $25.9 million of payments in 2021 and the first half of 2022,” the report summarized. “In the vast majority of these cases, the banks did not repay the customers that reported being scammed. Overall these three banks reported repaying customers in only 3,473 cases (representing nearly 10% of scam claims) and repaid only $2.9 million.”

Importantly, the report distinguishes between cases that involve straight up bank account takeovers and unauthorized transfers (fraud), and those losses that stem from “fraudulently induced payments,” where the victim is tricked into authorizing the transfer of funds to scammers (scams).

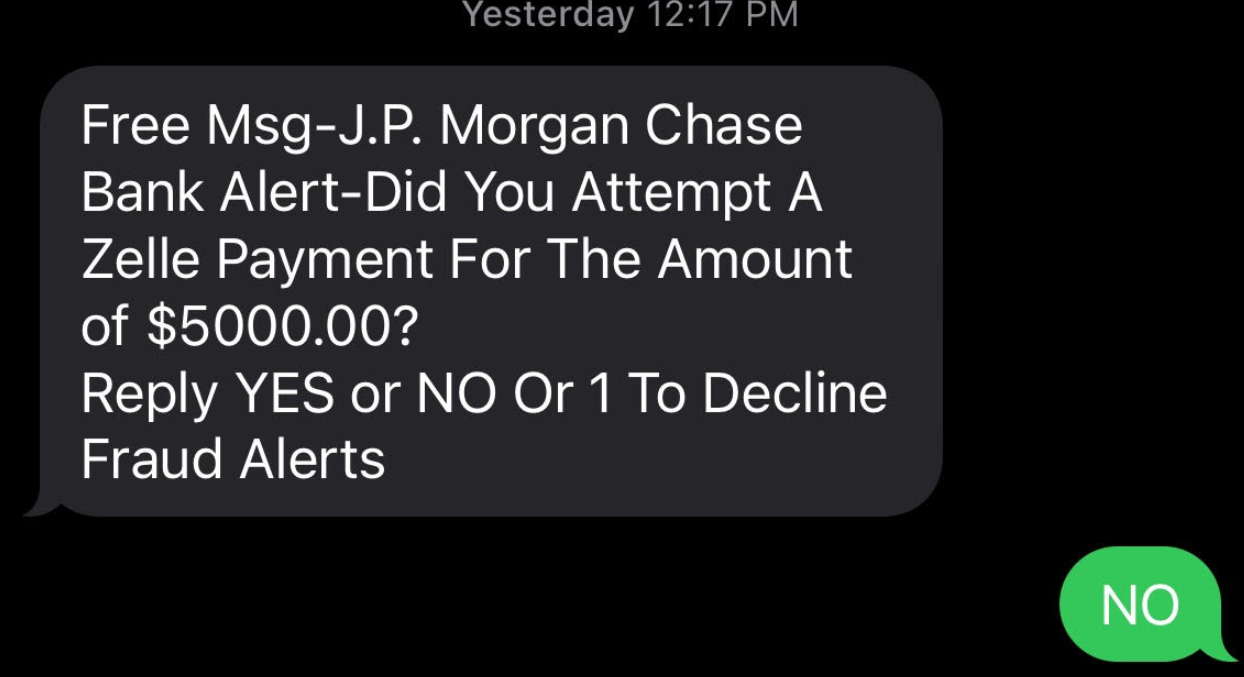

A common example of the latter is the Zelle Fraud Scam, which uses an ever-shifting set of come-ons to trick people into transferring money to fraudsters. The Zelle Fraud Scam often employs text messages and phone calls spoofed to look like they came from your bank, and the scam usually relates to fooling the customer into thinking they’re sending money to themselves when they’re really sending it to the crooks.

Here’s the rub: When a customer issues a payment order to their bank, the bank is obligated to honor that order so long as it passes a two-stage test. The first question asks, Did the request actually come from an authorized owner or signer on the account? In the case of Zelle scams, the answer is yes.

Trace Fooshee, a strategic advisor in the anti money laundering practice at Aite-Novarica, said the second stage requires banks to give the customer’s transfer order a kind of “sniff test” using “commercially reasonable” fraud controls that generally are not designed to detect patterns involving social engineering.

Fooshee said the legal phrase “commercially reasonable” is the primary reason why no bank has much — if anything — in the way of controlling for scam detection.

“In order for them to deploy something that would detect a good chunk of fraud on something so hard to detect they would generate egregiously high rates of false positives which would also make consumers (and, then, regulators) very unhappy,” Fooshee said. “This would tank the business case for the service as a whole rendering it something that the bank can claim to NOT be commercially reasonable.”

Sen. Warren’s report makes clear that banks generally do not pay consumers back if they are fraudulently induced into making Zelle payments.

“In simple terms, Zelle indicated that it would provide redress for users in cases of unauthorized transfers in which a user’s account is accessed by a bad actor and used to transfer a payment,” the report continued. “However, EWS’ response also indicated that neither Zelle nor its parent bank owners would reimburse users fraudulently induced by a bad actor into making a payment on the platform.”

Still, the data suggest banks did repay at least some of the funds stolen from scam victims about 10 percent of the time. Fooshee said he’s surprised that number is so high.

“That banks are paying victims of authorized payment fraud scams anything at all is noteworthy,” he said. “That’s money that they’re paying for out of pocket almost entirely for goodwill. You could argue that repaying all victims is a sound strategy especially in the climate we’re in but to say that it should be what all banks do remains an opinion until Congress changes the law.”

UNAUTHORIZED FRAUD

However, when it comes to reimbursing victims of fraud and account takeovers, the report suggests banks are stiffing their customers whenever they can get away with it. “Overall, the four banks that provided complete data sets indicated that they reimbursed only 47% of the dollar amount of fraud claims they received,” the report notes.

How did the banks behave individually? From the report:

-In 2021 and the first six months of 2022, PNC Bank indicated that its customers reported 10,683 cases of unauthorized payments totaling over $10.6 million, of which only 1,495 cases totaling $1.46 were refunded to consumers. PNC Bank left 86% of its customers that reported cases of fraud without recourse for fraudulent activity that occurred on Zelle.

-Over this same time period, U.S. Bank customers reported a total of 28,642 cases of unauthorized transactions totaling over $16.2 million, while only refunding 8,242 cases totaling less than $4.7 million.

-In the period between January 2021 and September 2022, Bank of America customers reported 81,797 cases of unauthorized transactions, totaling $125 million. Bank of America refunded only $56.1 million in fraud claims – less than 45% of the overall dollar value of claims made in that time.

–Truist indicated that the bank had a much better record of reimbursing defrauded customers over this same time period. During 2021 and the first half of 2022, Truist customers filed 24,752 unauthorized transaction claims amounting to $24.4 million. Truist reimbursed 20,349 of those claims, totaling $20.8 million – 82% of Truist claims were reimbursed over this period. Overall, however, the four banks that provided complete data sets indicated that they reimbursed only 47% of the dollar amount of fraud claims they received.

Fooshee said there has long been a great deal of inconsistency in how banks reimburse unauthorized fraud claims — even after the Consumer Financial Protection Bureau (CPFB) came out with guidance on what qualifies as an unauthorized fraud claim.

“Many banks reported that they were still not living up to those standards,” he said. “As a result, I imagine that the CFPB will come down hard on those with fines and we’ll see a correction.”

Fooshee said many banks have recently adjusted their reimbursement policies to bring them more into line with the CFPB’s guidance from last year.

“So this is heading in the right direction but not with sufficient vigor and speed to satisfy critics,” he said.

Seth Ruden is a payments fraud expert who serves as director of global advisory for digital identity company BioCatch. Ruden said Zelle has recently made “significant changes to its fraud program oversight because of consumer influence.”

“It is clear to me that despite sensational headlines, progress has been made to improve outcomes,” Ruden said. “Presently, losses in the network on a volume-adjusted basis are lower than those typical of credit cards.”

But he said any failure to reimburse victims of fraud and account takeovers only adds to pressure on Congress to do more to help victims of those scammed into authorizing Zelle payments.

“The bottom line is that regulations have not kept up with the speed of payment technology in the United States, and we’re not alone,” Ruden said. “For the first time in the UK, authorized payment scam losses have outpaced credit card losses and a regulatory response is now on the table. Banks have the choice right now to take action and increase controls or await regulators to impose a new regulatory environment.”

Sen. Warren’s report is available here (PDF).

There are, of course, some versions of the Zelle fraud scam that may be confusing financial institutions as to what constitutes “authorized” payment instructions. For example, the variant I wrote about earlier this year began with a text message that spoofed the target’s bank and warned of a pending suspicious transfer.

Those who responded at all received a call from a number spoofed to make it look like the victim’s bank calling, and were asked to validate their identities by reading back a one-time password sent via SMS. In reality, the thieves had simply asked the bank’s website to reset the victim’s password, and that one-time code sent via text by the bank’s site was the only thing the crooks needed to reset the target’s password and drain the account using Zelle.

None of the above discussion involves the risks affecting businesses that bank online. Businesses in the United States do not enjoy the same fraud liability protection afforded to consumers, and if a banking trojan or clever phishing site results in a business account getting drained, most banks will not reimburse that loss.

This is why I have always and will continue to urge small business owners to conduct their online banking affairs only from a dedicated, access restricted and security-hardened device — and preferably a non-Windows machine.

For consumers, the same old advice remains the best: Watch your bank statements like a hawk, and immediately report and contest any charges that appear fraudulent or unauthorized.

This entry was posted on Friday 7th of October 2022 02:46 PM

← Glut of Fake LinkedIn Profiles Pits HR Against the Bots

2 thoughts on “Report: Big U.S. Banks Are Stiffing Account Takeover Victims”

-

Taylor October 7, 2022

Not to mention, online banking in the US is hopelessly insecure. Authentication still based on SMS. My bank now allows the use of RSA Securid, for a $25 charge for the device, because apparently their IT staff is too incompetent to handle a mobile phone app like Google Authenticator (please don’t ask about FIDO)……but you can’t disable authentication with SMS! And this is advertised as a courtesy!

Reply → -

Ludovic Lalo October 7, 2022

You keep recommending using a non-Windows OS for online financial sites, but how much safer is Apple, Android, or Linux (two or three of which share the same foundation as I understand it) actually? The past year has revealed a multitude of vulnerabilities in those OSs too, some of which apparently existed for years. Moreover, if substantially more people gravitate to non-OS operating systems as daily drivers, namely for laptops/desktops, how “safe” will those OSs be when criminals start directing their energies to the market share leaders? It’s good to continually emphasis best online practices for individuals, but the discussion in your second to last paragraph is not germane to the gist of the article. The problem with Zelle is not its IT infrastructure (for now), but the fact that so many people are gullible and believe almost everything they see in “print” in texts and emails. Frankly, I do not understand why so many people fall for Zelle scams since I have never received a “fraud” call from any of my financial institutions or any type of call other than marketing call. Moreover, I question the mental competency of people who believe that they will be arrested the next day for non-payment of a fine or back taxes, having their utilities shut off the next day due to non-payment without any prior paper-based written notification, or really believe that any government/non-“mom and pop” business entity will only accept Zelle payments or “gift” cards as payment (the gift card as payment scam should be rejected on the basis of common sense alone). It seems to me that more people need to be made aware of how banks, brokerages, governments, utilities, etc. operate or basically made aware of their rights under the law when dealing with these entities so that they do not fall for scammers.

Reply →

Leave a Reply Cancel reply

Your email address will not be published. Required fields are marked *

Comment *

Name *

Email *

Website

Recommend

About Joyk

Aggregate valuable and interesting links.

Joyk means Joy of geeK